Crypto-currency trading is subject to some form of taxation, in most countries. These tax regulations vary by country, and we suggest researching your country’s tax laws to understand the specifics.

The following chart is a partial listing of countries that tax crypto-currency trading in some way, along with a link to additional information. Remember: Specific tax regulations vary per country; this chart is simply meant to illustrate if some form of crypto-currency taxation exists.

| COUNTRY | TAX STATUS | INFORMATION |

|---|---|---|

| United States | Taxed | IRS |

| Canada | Taxed | CRA |

| The United Kingdom | Taxed | HMRC |

| Germany | Taxed | BMF |

| Australia | Taxed | ATO |

| Japan | Taxed | LOC (English); NTA (Japanese) |

You can typically find more information about the specifics of your country’s taxation rulings on official government websites (such as IRS.GOV for United States taxation information). A compilation of information on crypto tax regulations in the United States, Canada, The United Kingdom, Germany, and Australia, which can be found here.

The Library of Congress published useful information in June 2018 with crytpocurrency taxation information for the following jurisdictions: Argentina, Australia, Belarus, Brazil, Canada, China, France, Gibraltar, Iran, Israel, Japan, Jersey, Mexico, and Switzerland. This document can be found here.

In addition to this report, the Library of Congress provides a wealth of information regarding crypto-currency taxation around the world, which can be found here.

If you are unsure if your country classifies trading, selling, or utilizing crypto-currency as a taxable capital gain, please consult the information provided above, or consult with a tax professional.

Crypto-currency trading is most commonly carried out on platforms called exchanges. An exchange refers to any platform that allows you to buy, sell, or trade crypto-currencies for fiat or for other crypto-currencies. There are a large number of exchanges which vary in utility – there are brokers, where you can use fiat to purchase crypto-currency at a set price and there are trading platforms, where buyers and sellers can exchange crypto with one another. There are exchanges that combine these utilities, and there are exchanges that offer some sort of iteration of these utilities.

One example of a popular exchange is Coinbase. On Coinbase, you can spend fiat to purchase Bitcoin, Bitcoin Cash, Litecoin, Ethereum, and Ethereum Classic. Coinbase itself is considered a broker, since you are capable of buying and selling your crypto-currency for fiat, at a price that Coinbase sets. Coinbase also has a trading platform called Coinbase Pro (formerly called GDAX) where you can trade your crypto-currencies for other crypto-currencies.

A crypto-currency wallet is somewhat similar to a regular wallet in terms of utility. A crypto-currency wallet does not actually store crypto, but rather stores your crypto encryption keys, communicates with the blockchain, and allows you to monitor, send, and receive your crypto. Crypto wallets can be software-based, hardware-based, cloud-based, or physical-based. Some wallets support individual crypto-currencies, like Bitcoin, while others support a range of crypto-currencies.

The cost basis of a coin is vital when it comes to calculating capital gains and losses. The cost basis of a coin refers to its original value. Here’s an example:

You buy 1 BTC for $6,500. The cost basis for that 1 BTC would then be what you paid, $6,500.

Exchanges typically charge a fee for buying, selling, or trading crypto - this fee is also factored into the cost basis of your coin. Consider the above example - if you paid $6,500 for 1 BTC and you were charged a $100 fee, your cost basis would be $6,600.

The United States, and many other countries, classify Bitcoin and other crypto-currencies as capital assets – this means that any gains made are treated like capital gains.

Bitcoin is classified as a decentralized virtual currency by the U.S. Treasury and as a commodity by the US Commodity Futures Trading Commission (CFTC). The IRS classifies Bitcoin as a property, which is the most relevant classification when it comes to figuring out your crypto-currency gains and losses.

A capital gain, in simple terms, is a profit realized. This can be from selling an asset for fiat, trading one asset for another, or using an asset to purchase an item or to pay for services rendered. Please refer to the “Taxable Events” section for a more in-depth look at the types of events that can incur capital gains.

A capital gains tax refers to the tax you owe on your realized gains. If you profit off utilizing your coins (i.e., trading, selling, etc.), those profits are taxed. Any losses you incur are weighed against your capital gains, which will reduce the amount of taxes owed.

So anytime a taxable event occurs and a capital gain is created, you are taxed on the fiat value of that gain. A simple example:

You buy 1 BTC for $6,000 USD and then later sell that 1 BTC for $10,000. You’ve made a profit, or capital gain, of $4,000. If your country is one of the many that taxes capital gains, you will have to pay a capital gains tax on the $4,000 capital gain.

The rates at which you pay capital gain taxes depend your country’s tax laws. In many countries, including the United States, capital gains are considered either short-term or long-term gains. The distinction between the two is simple to understand: long-term gains are gains that are realized on assets that are held for more than 1 year. Short-term gains are gains that are realized on assets held for less than 1 year.

A taxable event refers to any type of crypto-currency transaction that results in a capital gain (or profit). Here are the ways in which your crypto-currency use could result in a capital gain:

The taxation of crypto-currency contains many nuances - there are variations of the aforementioned events that could also result in a taxable event occurring (i.e., trading with coins acquired from a fork/split or buying something with crypto that you received for services rendered).

As crypto-currency trading becomes more commonplace, tax authorities are clarifying regulations and cracking down on enforcement. Some exchanges, like Coinbase, are have already been ordered by the government to turn over trading data for specific customers. It’s important that you are reporting any occurrence of a taxable event, even if the taxable event resulted in a loss.

Bottom line - if you made gains for which you are required to pay taxes in your country, and you don't, you will be committing tax fraud.

Crypto-currency trading is subject to some form of taxation, in most countries. The term “trading” encompasses many different actions involving crypto-currency. These actions are referred to as Taxable Events. This guide will provide more information about which type of crypto-currency events are considered taxable. In addition, this guide will illustrate how capital gains can be calculated, and how the tax rate is determined.

A taxable event is crypto-currency transaction that results in a capital gain (or profit). Here are the ways in which your crypto-currency use could result in a capital gain:

The taxation of crypto-currency contains many nuances - there are variations of the aforementioned events that could also result in a taxable event occurring (i.e., trading with coins acquired from a fork/split or buying something with crypto that you received for services rendered).

Simply buying a crypto-currency with fiat* does not create a taxable event. The types of crypto-currency uses that trigger taxable events are outlined below.

Keep in mind, it is important to keep detailed records of when you purchased the crypto-currency and the amount that you paid to acquire it. These records will establish a cost basis for these purchased coins, which will be integral for calculating your capital gains.

* The term “fiat” is used throughout this article. For those reading who are unfamiliar, the term “fiat” typically refers to a country's legal tender, such as USD or CAD.

Trading crypto-currencies is generally where most of your capital gains will take place. Here is a quick example to illustrate what “trading” refers to:

The above example is a trade. It can also be viewed as a SELL (you are selling .5 BTC and receiving 20 ETH in return) or a BUY (you are buying 20 ETH with a total cost of .5 BTC). Any way you look at it, you are trading one crypto for another.

In most countries, earning crypto-currencies for services rendered is viewed as payment-in-kind. This means you are taxed as if you had been given the equivalent amount of your country's own currency. So, for example, say your salary was paid in part cash and part Bitcoin, and each month you received $1000 worth of Bitcoins, you are taxed like you had just received $1000. If you are paid wholly in Bitcoins, say 5 BTC, then you would use the fair value. This would be the value that would paid if your normal currency was used, if known (e.g. $1000), otherwise you would use the price of Bitcoin at the time to establish your taxable income.

It's important to keep records of when you received these payments, and the worth of the coins at the time for two tax-related reasons: In terms of an income tax, you'll need to convert the values to fiat when filing income tax related documents (i.e., the W-2 form in the United States). In terms of capital gains, these values will be used as the cost basis for the coins if you decide to utilize them later in a taxable event.

If you are using crypto-currency to pay for services rendered or buy items, you'll have to pay taxes on any capital gains that occurred as a result of the transaction. Here's a non-complex scenario to illustrate this:

Paying for services rendered with crypto can be bit trickier. Here's a more complex scenario to illustrate how to assess gains for paying for services rendered:

Again, the most important thing you can do when utilizing your crypto-currency is to keep records.

Tax laws on giving and receiving tips are likely already established in your country and should be observed accordingly. You will similarly convert the coins into their equivalent currency value in order to report as income, if required. In the United States, gifts are usually not taxed unless they reach a certain threshold $15,000 in 2018)

As a recipient of a gift, you inherit the gifted coin's cost basis. This means that if someone paid $1,000 for 1 BTC and then gifted it to you, the cost basis is set at $1,000. So if you go on to sell that 1 BTC for $6,000, you'll incur a capital gain of $5,000, which will be taxed. It's important to ask about the cost basis of any gift that you receive.

Assessing the cost basis of mined coins is fairly straightforward. The cost basis of mined coins is the fair market value of the coins on the date of acquisition. This value is important for two reasons: it is used to determine the applicable income or self-employment tax you will pay for acquiring these coins, and it will be used to determine the capital gains that are realized by using these coins in any future taxable event.

Keep in mind, any expenditure or expense accrued in mining coins (i.e., hardware or electricity) does not play a role in calculating the cost basis. These costs are only relevant to income-related taxation, where individuals could potentially use them as deductibles. Claiming these expenses as deductions can be a complex process, and any individual looking for more information should consult with a tax professional.

Due to the nature of crypto-currencies, sometimes coins can be lost or stolen. The Mt. Gox incident is one wide-spread example of this happening. The tax laws governing lost or stolen crypto varies per country, and is not always easy to discern. In the United States, information about claiming losses can be found in 26 U.S. Code § 165 - Losses.

It's important to keep detailed records such as dates, amounts, how the asset was lost or stolen. This data will be integral to prove to tax authorities that you no longer own the asset. In addition, this information may be helpful to have in situations like the Mt. Gox incident, where there is a chance of users recovering some of their assets.

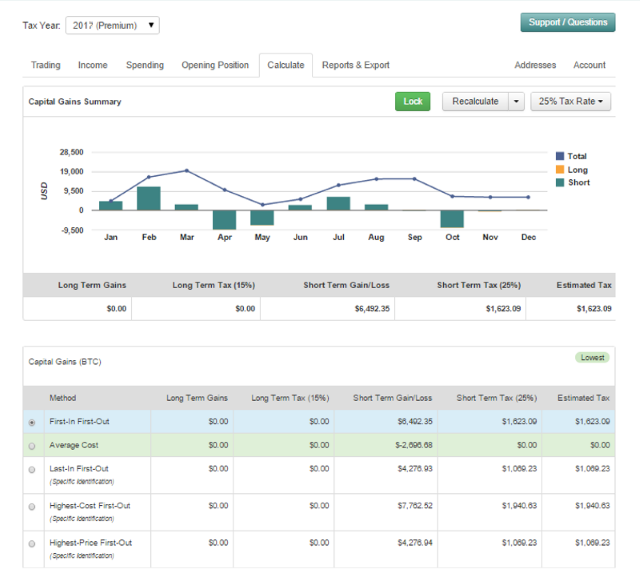

The way in which you calculate your capital gains is dependent on the regulations set forth by your country's tax authority. One of the most commonly used methods is FIFO (First-In-First-Out). FIFO means that your gains will be calculated by using your oldest coins' cost basis (“first-in”) to calculate your most recent trade or transaction (“first-out”). Here is a brief scenario to illustrate this concept:

January 1st, 2018: You buy 1 BTC for $6,000 USD

January 5th, 2018: You buy 1 BTC for $8,000 USD

January 10th, 2018: You sell 1 BTC for $10,000 USD

Using FIFO, capital gains would be realized on the 1 BTC you sold on January 10th, 2018 using the 1 BTC you bought on January 1st, 2018. Since you paid $6,000 USD on January 1st for 1 BTC and then sold 1 BTC for $10,000 USD on January 10th, your capital gain would be $4,000 USD, which you would pay taxes on.

Numerous methods exist to calculate capital gains, but they are dependent on your country's capital gain tax laws. Canada, for example, uses Adjusted Cost Basis.

In the United States, FIFO is the most commonly used method of capital gains calculations. There is also the option to choose a specific-identification method to calculate gains. These methods include LIFO, HCFO, HPFO, LCFO, LPFO, and CCFO. Calculating your gains by using an Average Cost is also possible.

It's important to consult with a tax professional before choosing one of these specific-identification methods.

Prior to 2018, the tax laws in the United States were unclear whether crypto-currency capital gains qualified for like-kind treatment. In simplified terms, like-kind treatment did not trigger a tax event when exchanging crypto for other crypto; a tax event would only be triggered when selling crypto for fiat. If you are still working on your crypto taxes for 2017 and earlier, it is important that you consult with a tax professional before choosing to calculate your gains using like-kind treatment.

At the end of 2017, a tax-bill was enacted that clearly limits like-kind exchanges to real estate transaction. This means that like-kind is no longer a potential way to calculate your crypto capital gains in the United States 2018 and beyond.

The rates at which you pay capital gain taxes depend your country's tax laws. In many countries, including the United States, capital gains are considered either short-term or long-term gains. The distinction between the two is simple to understand: long-term gains are gains that are realized on assets that are held for more than 1 year. Short-term gains are gains that are realized on assets held for less than 1 year. An example of each:

Short-Term: You buy 1 BTC on January 1st, 2018 for $6,000 USD. You sell the 1 BTC on January 2nd, 2018 for $6,500 USD. You have realized a short-term gain of $500 USD, which is subject to your short-term capital gains tax.

Long-Term: You buy 1 BTC on January 1st, 2018 for $6,000 USD. You sell the 1 BTC on April 2nd, 2019 for $8,500 USD. You have realized a long-term gain of $2,500 USD, which is subject to your long-term capital gains tax.

Long-term tax rates are typically much lower than short-term tax rates. In the United States, for example, short-term tax rates are based off of an individual's income tax rate, which range between 10% and 37% (2018). Long-term tax rates in the United States are also based on an individual's income tax rate, but range between 0% and 20% (2018).

Ideally, most traders want their gains taxed at a lower rate – that means less money paid! However, in the world of crypto-currency, it is not always so simple. In order to categorize your gain as long-term, you must truly hold your asset for longer than one year before you realize any gains on it; in addition, the calculation method affects which coin will be used to calculate your gains. Here's a scenario:

You buy 1 BTC in 2015 for $500 USD. You also buy 1 BTC on January 1st, 2018 for $6,000 USD. You decide to sell 1 BTC on April 1st, 2018 for $10,000 USD. If using a FIFO calculation method, your gain would be calculated using the 1 BTC you purchased in 2015. This would trigger a long-term gain of $9,500.

If you calculated your 1 BTC April 1st, 2018 sale using LIFO, you would calculate the gain using the 1 BTC you purchased on January 1st, 2018. This would trigger a short-term gain of $4,000 USD.

Calculating crypto-currency gains can be a nuanced process. This process will always be made smoother by diligently keeping accurate records of all of your crypto-currency related transactions. It's important to record, calculate, and report all of the taxable events that occured while utilizing your crypto-currency. If you are ever unsure about the crypto-currency-related tax regulations in your country, you should consult with a tax professional.

Bitcoin.Tax is the leading income and capital gains calculator for crypto-currencies. You import your data and we take care of the calculations for you. We offer a variety of easy ways to import your trading data, your income data, your spending data, and more. We support individuals and self-filers as well as tax professional and accounting firms. Anyone can calculate their crypto-currency gains in 7 easy steps.

Bitcoin.Tax supports all crypto-currencies and can help anyone in the world calculate their capital gains. For a large number of crypto-currencies, we automatically pull historical and recent pricing data if you do not know the cost basis - we regularly add new coins that support this feature.

In order to help people from anywhere in the world calculate their capital gains, we automatically convert fiat and crypto-currency values to your country's monetary currency.

Your account's default currency will be based on the country you select during sign-up.

Bitcoin.Tax offers a variety of plans depending on how many trades you want to import and calculate. Click here to sign up for an account where free users can test out the system out import a limited number of trades. Individual accounts can upgrade with a one-time charge per tax-year. Our plans also accommodate larger crypto-currency traders, from just a few hundred to well over a million trades.

We also have accounts for tax professionals and accountants. Click here for more information about business plans and pricing.

Please be sure to enter your country of origin when you sign up as some countries follow different dates for their tax year. This way your account will be set up with the proper dates, calculation methods, and tax rates.

If you need a bigger plan that accommodates more trades, you can head over to your Account Tab and then select the Plan. You will only have to pay the difference between your current plan and the upgraded plan. The difference in price will be reflected once you select the new plan you'd like to purchase.

Bitcoin.Tax offers a number of options for importing your data. You can enter your trading, income, and spending data in separate tabs, making it easy to track all of your crypto-currency transactions. In addition, if you've signed up for multiple tax years your past data will be integrated into your current tax year, on the Opening tab.

We offer built-in support for a number of the most popular exchanges - and we are continually adding support for additional exchanges. Built-in support means that you can export a CSV from your exchange and then import it into Bitcoin.Tax. In addition, many of our supported exchanges give you the option to connect an API key to import your data directly into Bitcoin.Tax. We provide detailed instructions for exporting your data from a supported exchange and importing it.

Here is a list of exchanges with built-in support:

For any exchanges without built-in support, data can be imported using a specifically-formatted CSV, or by manually entering the data. Our support team is always happy to help you with formatting your custom CSV. You can also let us know if you'd like an exchange to be added

Bitcoin.Tax allows users to compare capital gains/losses using different cost-basis methodologies, including FIFO, LIFO, and averaging/adjusted cost basis with or without like-kind treatment.

Please note, as of 2018, calculating crypto-currency trades using like-kind treatment is no longer allowed in the United States.

Download capital gains reports as CSV, Schedule D 8949 PDF and 8949 attachable statement. Import reports into TurboTax, H&R Block, TaxACT, Drake Software, CCH, or any tax software that supports TXF files. Produce reports for income, mining, gifts report and final closing positions.

Bitcoin.Tax prides itself on our excellent customer support. Our support team goes the extra mile, and is always available to help. Click here to access our support page. Please note that our support team cannot offer any tax advice.

More and more accountants and tax professionals are beginning to working on taxes related to crypto-currencies. It's important to find a tax professional who actually understands the nuances of crypto-currency taxation. Bitcoin.Tax has put together a page of tax attorneys, CPAs, and accountants who have registered themselves as knowledgeable in this area and might be able to help.

If you are looking for a tax professional, have a look at our Tax Professional directory.

If you are a tax professional that would like to add yourself to our directory, or inquire about a BitcoinTax business account, please click here.

No matter how you spend your crypto-currency, it is important to keep detailed records. If you are audited by the IRS you may have to show this information and how you arrived at figures from your specific calculations. Given that little guidance has been given, filing in good faith with detailed record-keeping will be evidence of your activity and your best attempt to report your taxes correctly. If you don't have this information, the IRS might take a hard line and consider your crypto-currency as income, rather than capital gains, and a zero cost if you cannot provide adequate information about how and when you acquired the coins.

Bitcoin.Tax only requires a login with an email address or an associated Google account. We don't hold or store any other information about you/ If you decide to upgrade, you can pay woth a credit card or anonymously with Bitcoin. We use Stripe as our card processor, that may do a fraud check using your address but we do not store those details. Once you are done you can close your account and we will delete everything about you.

We do NOT provide any information about you or your capital gains to the IRS.